Whether it’s for business or student, or simply an amount of money that we are lending to a relative, loans are a part and parcel of daily life and so is the need for a loan agreement.

If you wish to learn more about loan agreements such as what they are, why and where they are used, and what they comprise of, this article will answer all your doubts. Simply read on, and you’ll be a much more informed lender or borrower within a few minutes.

Have you been searching for a ready to use loan contract template? We have got that covered as well. Download our simple loan agreement template and use it at no extra charge!

Alternate Names for Loan Agreement

There are various ways of referring to a loan agreement. Some people call it a ‘promissory note’, while others may refer to it as a ‘term loan’ document. You may also find people calling it an ‘IOU’ (I Owe You) document or a ‘Note Payable’.

All these terminologies mean the same thing and you can use this loan agreement template.

What Is a Loan Agreement?

It is a legal document between the borrowing and the lending party that stipulates the conditions of the loan and the promises made by both the parties. Its purpose is to protect both the parties in case a dispute arises and the court has to step in

In general, any loan agreement template explicitly lists out the basic loan terms like the loaned amount and the agreed-upon interest rate, repayment timeline, collateral (if it’s there), default penalties, along with any specific terms and conditions.

What Can You Use a Loan Agreement for?

A loan agreement is used for a variety of loans. There is a loan agreement between individuals, between businesses, or between business and an individual. Some top of the mind examples of its applications are:

- Loans taken by students for funding tuition or other education-related expenses.

- Loans to fund the purchase of any item like a car, electronic appliance, furniture, etc.

- Loans related to real estate, such as the purchase of a home or property.

- Loans for business expansion such as capital investment in your factory, startup, etc.

- Loans or simple IOUs between relatives, friends or colleagues.

Why do People Use a Loan Agreement?

Loan agreements are useful because they clearly outline what each of the parties is agreeing to, and what are their responsibilities. A loan agreement form is a binding contract and it formalizes the loan process.

It protects the lender’s interest as it enforces the borrower’s promise of repaying the money. It also makes it evident that the money being exchanged is a loan and not a gift.

If you are lending to your friends and family, a loan agreement can prevent later tussles over the lending terms. Loan agreement is also very useful for the borrowers as it clarifies the lender’s expectations and helps you plan your payments.

Check out our free loan agreement template and you can see that its various terms and clauses are thorough and remove any scope of misinterpretation

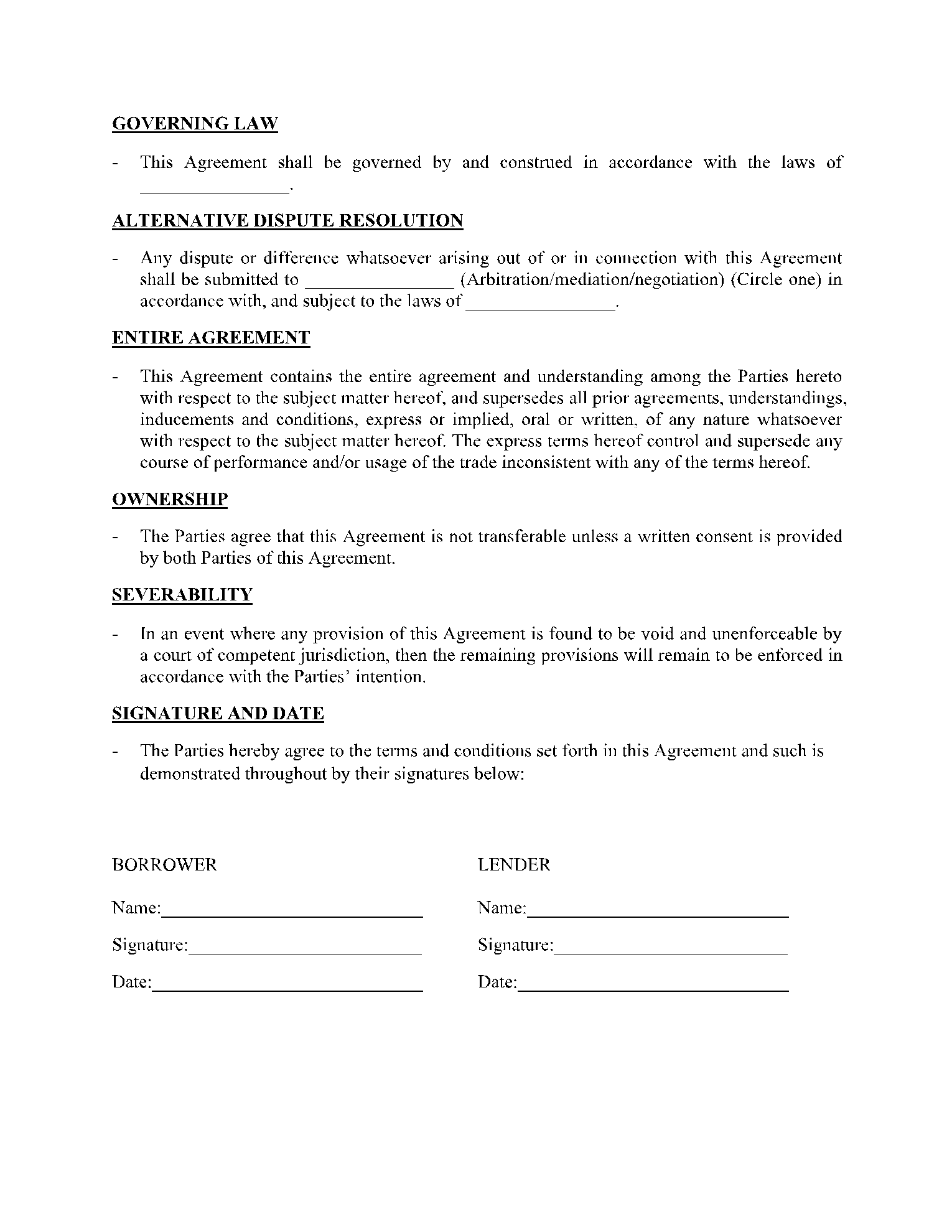

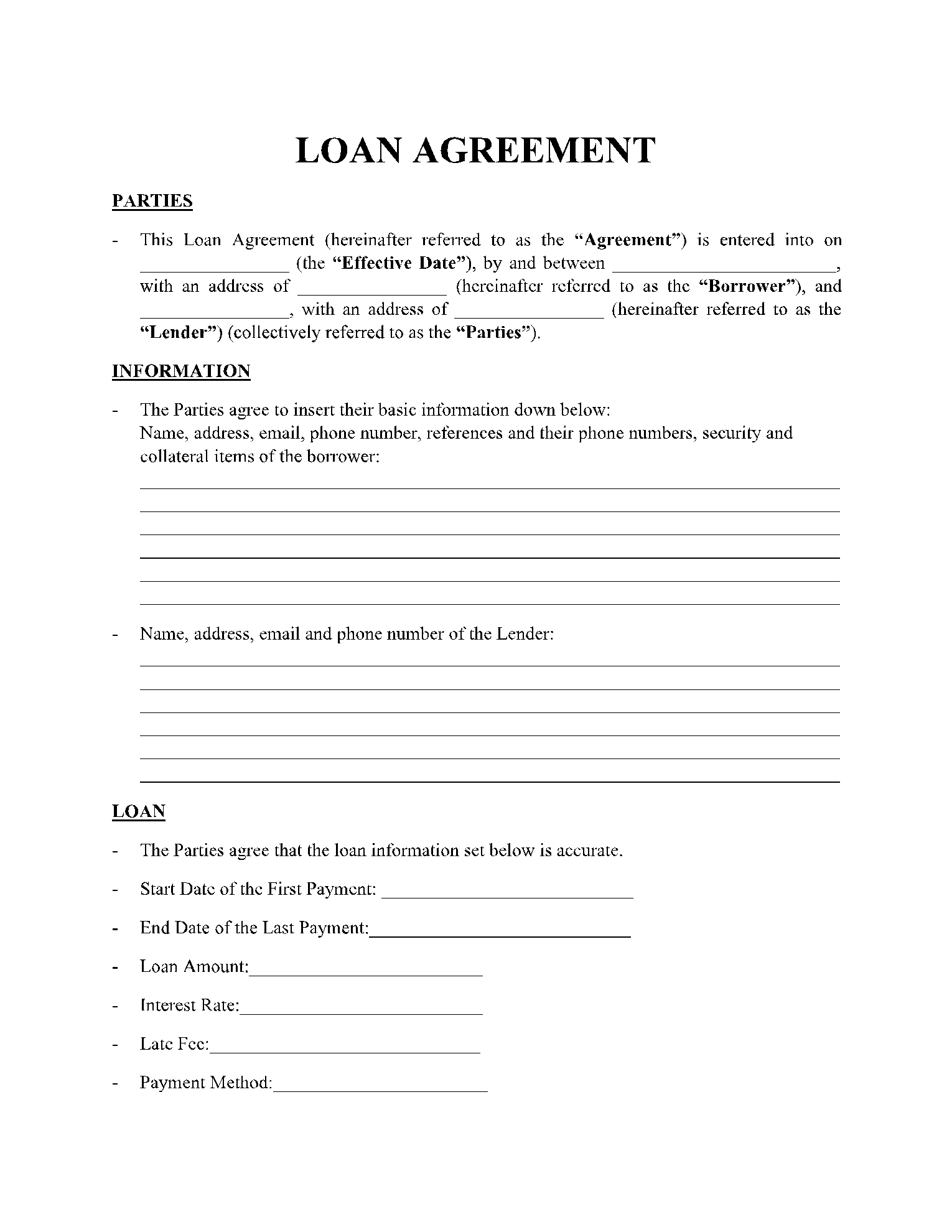

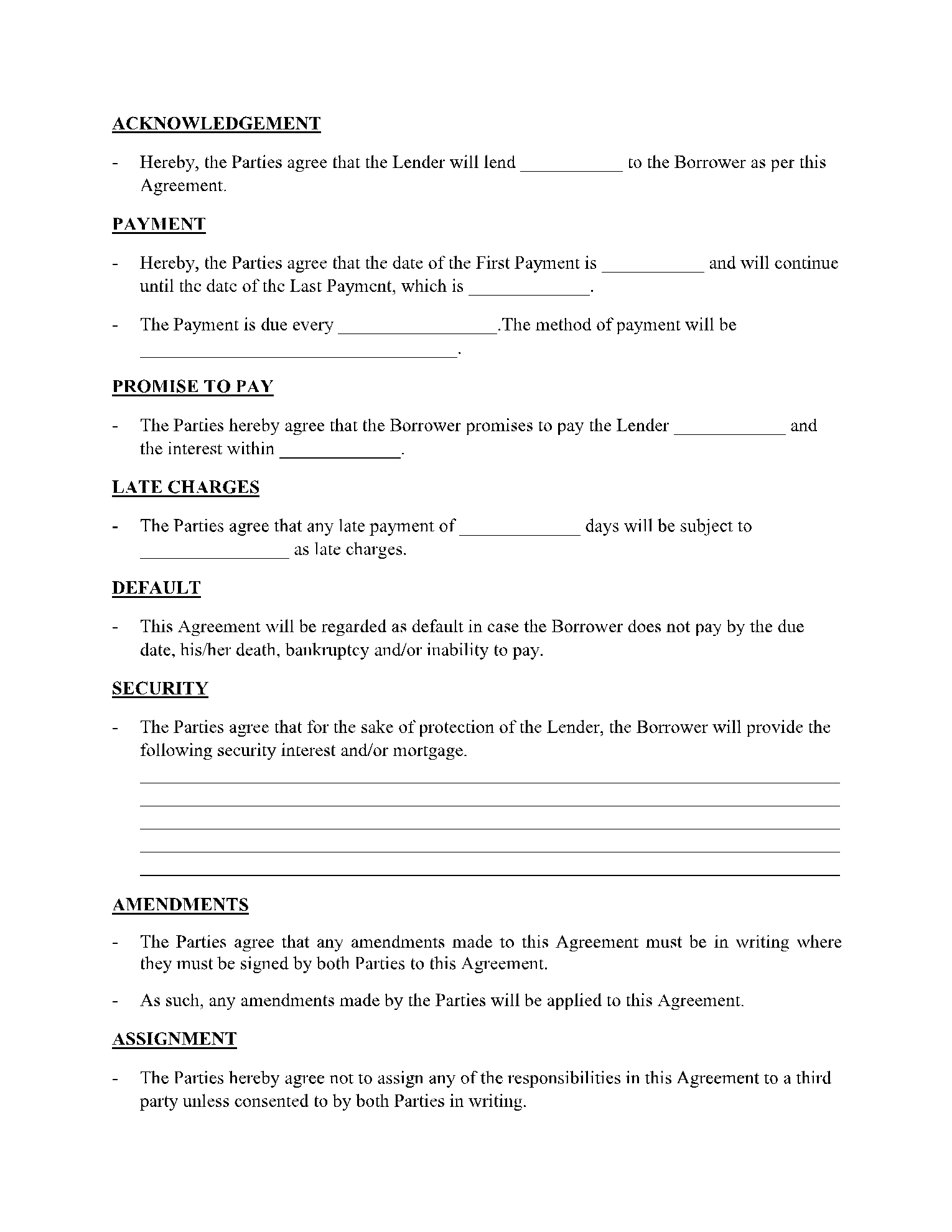

What Are Included in a Loan Agreement?

Every loan agreement template will cover some basic points:

- Loan Amount: It stipulates the amount being exchanged, applicable interest rates, and how it will be computed (simple or compound).

- Payment method: This means how the lender will receive money back from the borrower.

- Repayment schedule: It lists out the number of installments, their dates, and amount.

- Details of lender and borrower along with their addresses

- Collateral: Some kind of security can be decided in advance in case the borrower is unable to repay the loan.

How Is a Loan Agreement Different from a Promissory Note?

Both the loan agreement and the promissory note are formal contracts that clarify the lending terms between the lender and the borrower. However, there are certain differences in their applications and hence minute differences in their loan template as well.

Promissory note is used for simple loans while a loan agreement typically involves an extensive payment schedule and terms. Thus, a loan agreement template is much more detailed than a promissory note.

Both the borrower and the lender need to sign a loan agreement while a promissory note needs only be signed by the borrower.

Conclusion

These agreements are useful for both the parties as they clearly outline every term and condition related to the loan. If you are entering into a loan, please download and use the free loan agreement template on CocoSign.

Are you also seeking something other than a loan agreement template? Whether it’s related to real estate, business, financial, or family-related requirements, we are into knowledge sharing and providing ready-to-use templates for all kinds of purposes.

So, check out our website, and take a step towards securing your interests!

Loan Agreement FAQ

-

Does the loan agreement need signatures of witnesses?

No, you don’t always need to get a loan agreement signed from witnesses. It basically depends on where you are entering into the loan and what that region’s judiciary law states.

Sometimes laws do require a witness, or even a public notary official to attest your loan agreement.

Irrespective of the legal mandates, we feel that it is advantageous to get an objective outsider to witness your agreement being signed as it lends a greater credibility if you ever enter into a legal dispute.

-

What is interest and how is it calculated?

Lenders levy an Interest amount on their borrowers in return for using their money. This is the lender’s fee for the inconvenience he is incurring and the risk he is taking in this exchange.

Some people believe that the interest necessarily needs to be charged in a loan agreement. However that is not so. You may choose to have zero interest loans as well.

Generally interest rates are specified as a percentage. 5% interest rate means 5% of the borrowed amount. Interest rates may be calculated at a specified period of time, say monthly, quarterly, annually, etc. Typically the rate of interest mentioned is the annual rate.

-

Do I have to get an independent contractor agreement for my company’s employees?

No, there is no need for an independent contractor agreement for the employees of a company. The purpose of these contracts is to differentiate the contractor from an employee.

-

What are the different types of payment options?

Loan repayment can be settled in four different ways, which include lump-sum, periodic payments of specific amounts, regular interest payments only, and regular interest and principal payments.

-

What is the meaning of a loan agreement governing law?

You are bound by the laws of the jurisdiction in which you enter into the loan agreement. It is clearly and explicitly stated in the Governing Law Clause of a loan agreement template.

Typically, the lender and the borrower agree to select the law of the lender’s jurisdiction. Sometimes when you are taking a loan to purchase some assets, the jurisdiction region could pertain to the location of these assets.

-

Is it necessary to keep collateral in a loan?

No, it is not essential to keep collateral in your loan agreement form. However it is advisable to do so.

If the loan without collateral gets defaulted, you will have to take the matter up with the court. Moreover, the judgment is enforceable only against specific assets of the borrowing party.

On the other hand, if a collateral was agreed upon in the agreement, you are entitled to seize it and sell it to recover the due amount.