As a property developer, it's crucial to sustain all of your options in mind when it involves selling or buying a brand-new property. There are numerous non-conventional financing methods that may offer unique benefits, regardless of what side of the deal you're on.

Among these opportunities is seller financing, a process that essentially eliminates the middleman and allows buyers and sellers to barter more directly than a conventional loan. Keep reading to find out the basics of a seller financing addendum and how to write it!

What Is a Seller Financing Addendum?

If you would like to sell a house quickly or buy a house at a reduced price, then you would possibly consider a seller financing addendum. This is often a specific tool that the vendor uses to form an acquisition in her house during difficult financial times.

Seller financing is strictly what it sounds like: the vendor provides the financing instead of a bank or mortgage lender. Seller financed homes are acquired by the client the identical way the other property is bought and sold, except without directly browsing the bank. Instead, the previous owner will act because the bank can receive payments directly from the vendor.

The seller financing addendum is an addition to the typical sale and buy agreement, severely limiting the seller's accountability during and after the sale process. As an example, the vendor addendum might limit damages to which the buyer is entitled within the event seller fails to disclose some problem with the property.

Seller financing could be a land agreement within which the vendor handles the mortgage process rather than a financial organization. Thus, instead of applying for a standard bank mortgage, the client signs a mortgage with the vendor. The seller financing agreement is also called owner financing and a purchase-money mortgage.

Download Free Our Seller Financing Addendum Template Now!

Running out of money or if you're tight on budget, there is no other option better than to go for a document for seller financing addendum. Our template is available for free, and you can access it by downloading it with a single click today.

Why Needs a Seller Financing Addendum?

This method of house selling allows the vendor to supply her home to buyers outside of the normal range. Because the seller is willing to supply a mortgage, or a part of the mortgage, the sale is probably going to be completed more quickly.

A seller financing addendum is a flexible method of agreeing to a property purchase because the seller and buyer need only to barter repayment terms. A seller financing addendum provides supplementary terms for a buying deal involving the buyer being provided by the required basic funds to get the house i.e. a loan.

Although most buyers obtain financing from local mortgage lenders, sometimes sellers offer to provide the needed money to cut back the number of your time. And they get a return on their investment from the interest rate and receive certain tax benefits.

This is often also advantageous to any buyers who seek less stringent qualification requirements, flexible down payments, and fewer closing costs.

Using a seller finance addendum can facilitate a seller to sell your house more quickly if the economy is experiencing a downturn and mortgage lenders are tightening their lending requirements. Seller finance addendums specify the terms of the mortgage when a home-owner is providing the financing for the client.

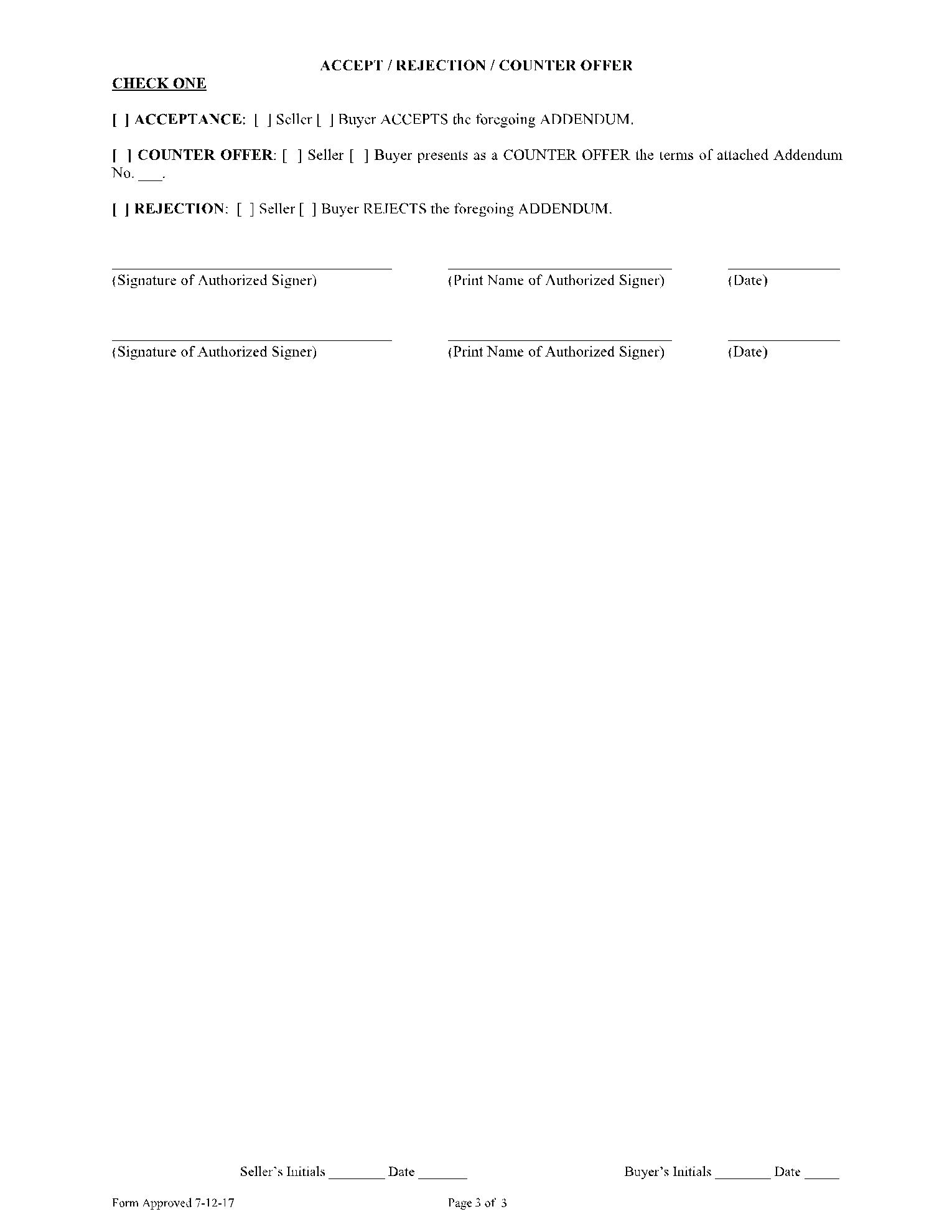

What Is Included in a Seller Financing Addendum?

Following are the contents that are advised to be included in a seller financing addendum,

- The title for the seller financing addendum. This generally includes the summary of this addendum’s purpose.

- The date on which the seller financing addendum was created.

- Mention some specifics required by this addendum for the contract.

- Deliver the required financial information.

- Type of loan either amortized, interest-only, balloon, or adjustable-rate.

- Mention the terms for the loan.

- Include the amount being financed, the interest rate of the loan, and the rate of the purchaser's monthly payment.

- A promissory note to be submitted into the public record.

- Name of the seller and buyer who signed the agreement.

- The full address of the premises, including zip code, city or town, and county of the rental property.

- The contact information, including authorized signatures.

Download Free Our Seller Financing Addendum Template Now!

Running out of money or if you're tight on budget, there is no other option better than to go for a document for seller financing addendum. Our template is available for free, and you can access it by downloading it with a single click today.

Conclusion

By financing the damage, a seller can accept a suggestion from a buyer that doesn't qualify for a standard mortgage. Mentioned above are all the basics you need to learn about a seller financing addendum. We hope it was helpful to you.

If you are interested to learn more about seller financing agreements or similar purchase contracts, you can visit our website CocoSign, where we have got several free templates of property purchase agreements including seller financing addendum.

DOCUMENT PREVIEW

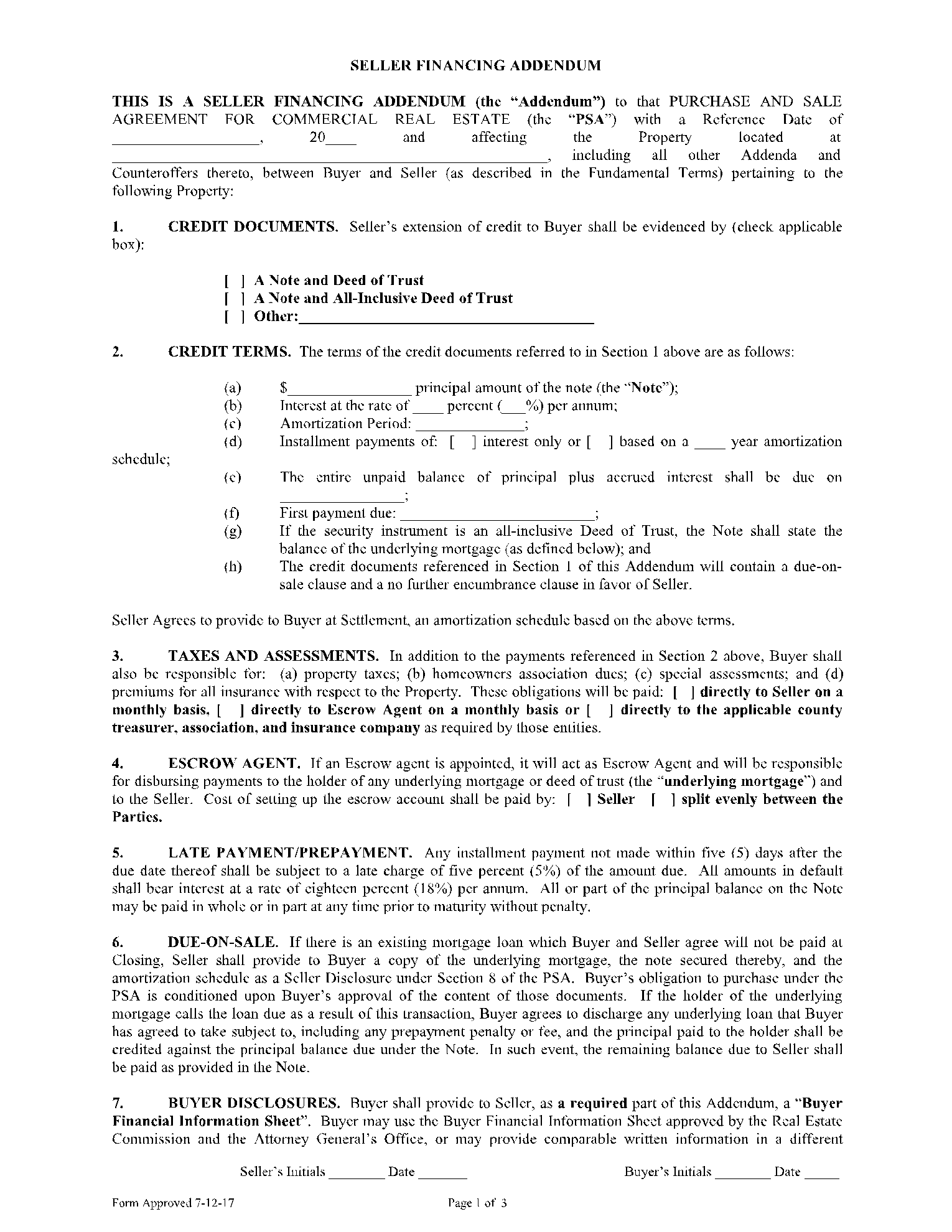

SELLER FINANCING ADDENDUM

I. The Parties. This Seller’s Financing Addendum (“Addendum”) is made between _______________________ (“Buyer”) and _______________________ (“Seller”) to be incorporated and made a part of the Purchase and Sale Agreement for the property located at _______________________, City of _______________________, State of _______________________ (“Property”) with an Effective Date of _______________________, 20____ (“Agreement”).

II. Effective Date. _______________________, 20____ (“Effective Date”).

III. Mortgage. As part of the Purchase Price stated in the Agreement, Buyer shall execute and deliver to Seller at closing a promissory note and purchase money mortgage that is a ☐ First (1st) Mortgage ☐ Second (2nd) Mortgage on the Property in the amount of $_______________________ at an interest rate of ____% per annum in accordance with this Addendum as follows:

IV. Buyer’s Credit Information. Within ____ days after the Effective Date of this Addendum, the buyer shall furnish all credit, employment, and financial information reasonably required by Seller (“Credit Information”).

V. Seller’s Approval. Seller shall deliver written notice to the Buyer within ____ days if their Credit Information is approved or rejected. If no written notice is delivered, Buyer shall be considered approved for Seller's financing under the terms of this Addendum.

If Buyer’s Credit Information is rejected by the Seller, any earnest money deposited as part of the Agreement shall be returned to the Buyer unless otherwise stated.

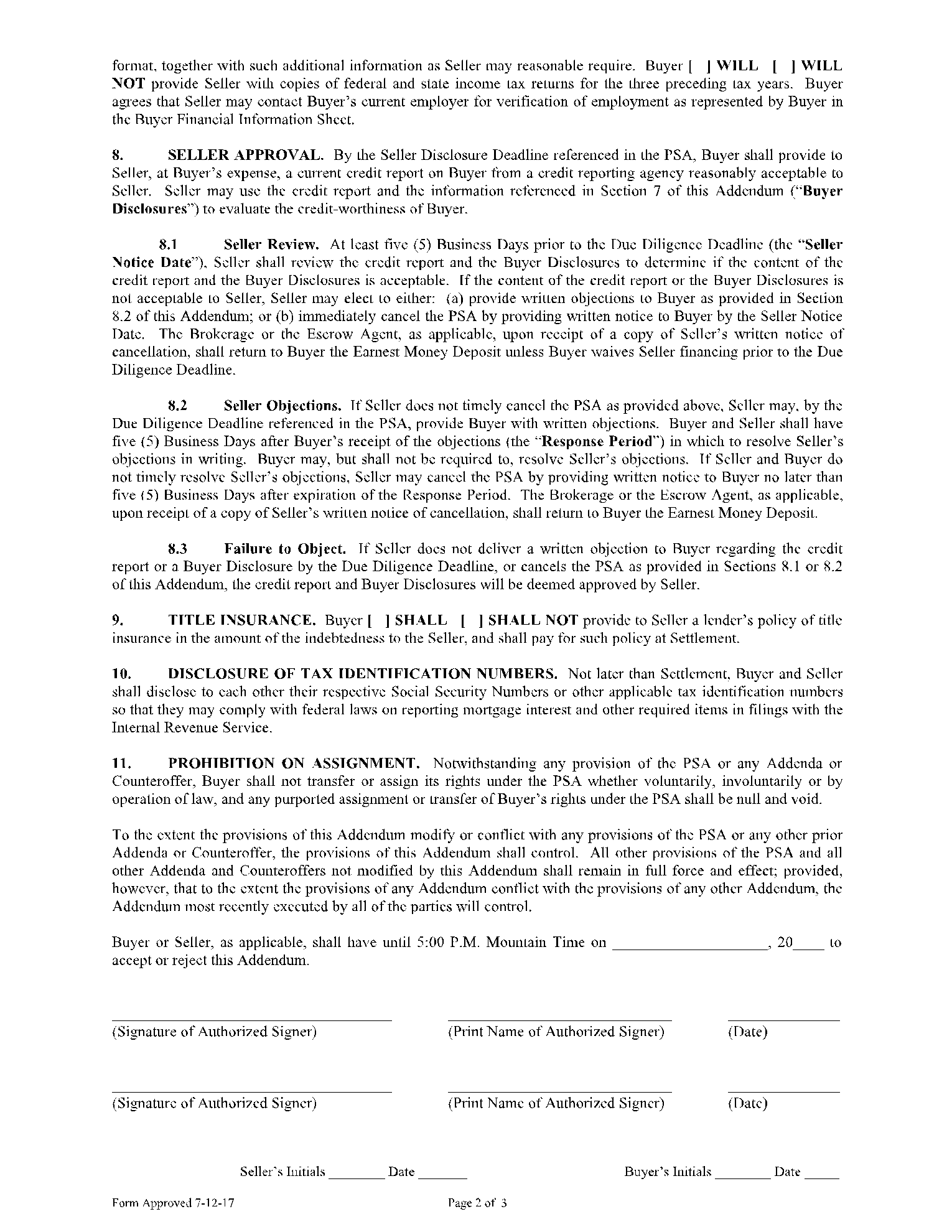

VI. Financing Terms. The Seller’s financing terms shall be: (Choose One)

☐ Amortized Loan. Fully Amortized for a term of ____ ☐ Months ☐ Years.

☐ Interest Only. An interest-only mortgage loan that complies with the requirements of Dodd-Frank legislation and requires monthly payment with the entire principal balance and accrued interest due in full on _______________________, 20____.

☐ Balloon Mortgage. A balloon mortgage that complies with the requirements of Dodd-Frank and initially amortized for a term of ____ ☐ Months ☐ Years with the remaining principal balance and accrued interest due in full on _______________________, 20____.

☐ Adjustable Rate Mortgage. An adjustable rate mortgage loan that shall be for a term of ____ ☐ Months ☐ Years with the interest rate adjustments as follows:

(1) The initial annual interest rate may change after ____ years and thereafter every ____ years. Each date on which the interest rate changes is called a “Change Date”; and

(2) The interest rate adjustments shall be based on a widely available index identified in (3) below. As of each Change Date, the new interest rate will be calculated by adding ____ percentage (basis) points to the then current index; however, the difference between the interest rate paid during the preceding twelve months and the new interest rate ☐ shall not be limited ☐ shall be limited to a change in the interest rate of ____ percentage (basis) points, and the lifetime interest rate change from the initial annual interest rate ☐ shall not be limited ☐ shall be limited to ____ percentage (basis) points.

(3) The widely available index to be used to calculate interest rate adjustments shall be:

☐ The weekly average yield on the United States Treasury securities adjusted to a constant maturity of one year, as made available by the Federal Reserve Board on the date 45 days before each Change Date.

☐ Other. _________________________________________________________

VII. Taxes. All real property taxes ☐ Shall be Escrowed ☐ *Shall Not be Escrowed. *If not escrowed, proof of payment shall be furnished at the request of the mortgage holder within five (5) days.

VIII. Insurance. All real property and liability insurance ☐ Shall be Escrowed ☐ *Shall Not be Escrowed. *If not escrowed, proof of payment shall be furnished at the request of the mortgage holder within five (5) days.

IX. Pre-Payment. (Choose One)

☐ There shall not be a pre-payment penalty. Buyer may pay the total amount of the mortgage at any time free of penalties or fees.

☐ There shall be a pre-payment penalty if the balance of the mortgage is paid before the last payment date. Penalty for such pre-payment shall be _________________________________.